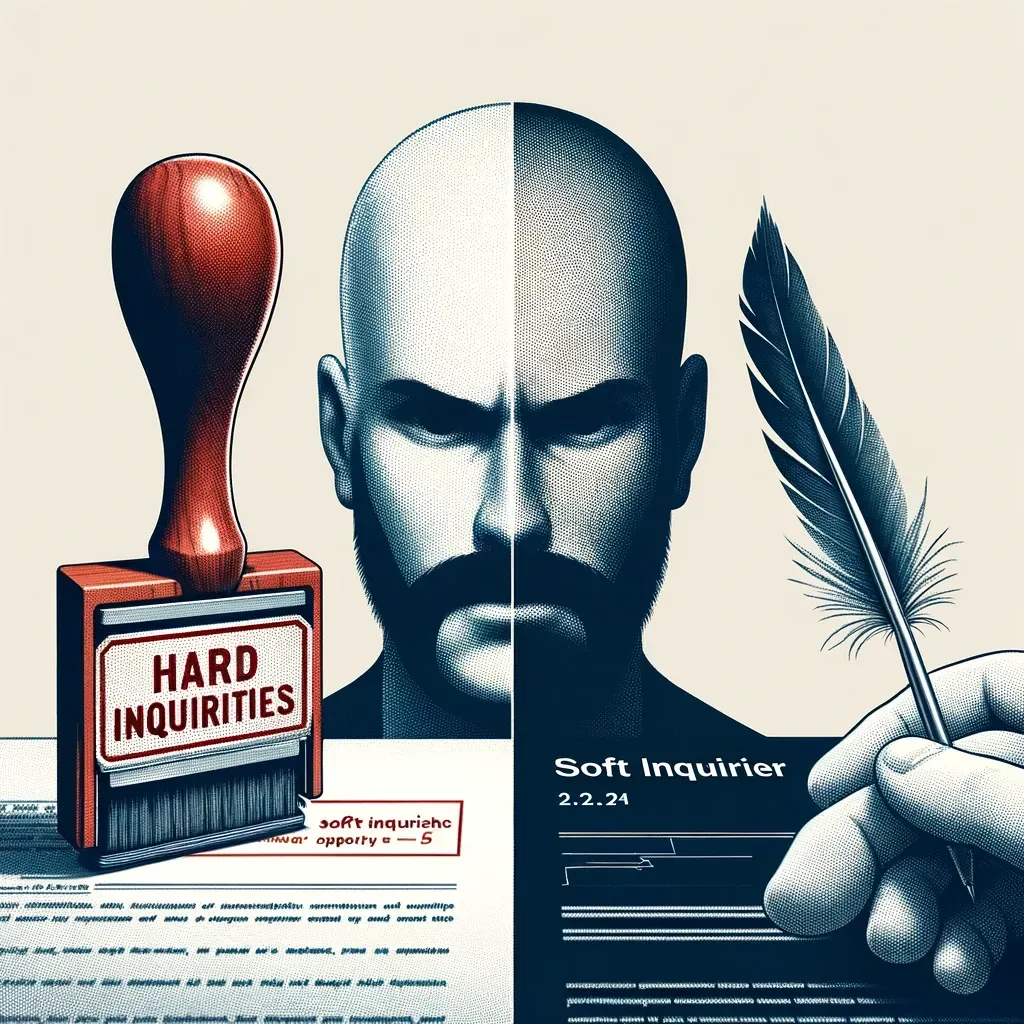

How do hard inquiries and soft inquiries differ?

Soft Inquiries Have No Impact On Your Credit, Hard Inquiries Can Lower Your Credit Score And Make You Appear Risky To Lenders

Diving into the world of credit inquiries is akin to stepping into a detective story, where every clue (or in this case, inquiry) can lead to a different outcome. With 15 years on the credit scene, I've seen my fair share of plot twists and turns, especially when it comes to distinguishing between hard inquiries and soft inquiries. Let's unravel this mystery with a touch of humor and clarity.

The Tale of Two Inquiries

Imagine you're at a grand ball (stay with me here), and you've caught the eye of two suitors: one is a bit more forward (let's call them Hard Inquiry), and the other is more discreet (we'll name them Soft Inquiry).

Hard Inquiry, much like our forward suitor, makes a bold move. They're the type to ask for a dance in front of everyone, leaving a mark on your social standing (or in the real world, your credit report). This occurs when you actually apply for credit, be it a mortgage, a credit card, or an auto loan. It signals to others (lenders) that you're looking for new credit, which can be a turn-off if you're playing the field too aggressively. Each hard inquiry might slightly lower your credit score, as it suggests you might be taking on new debt. However, this impact is typically minor and short-lived, fading over time.

Soft Inquiry, on the other hand, is the discreet suitor who admires you from afar or maybe asks a mutual friend about you. These inquiries happen when someone checks your credit but you haven't applied for new credit. This could be you checking your own score, a credit card issuer pre-approving you for an offer, or a landlord peeking at your credit before renting you an apartment. Soft inquiries are like whispers in the night; they don't affect your credit score, as they're not associated with a new credit application.

The Plot Thickens: Impact on Your Credit

Hard inquiries can stay on your credit report for up to two years, but their impact diminishes over time. Think of them as footprints in the sand, gradually washed away by the waves. Having too many in a short period can make lenders wary, as it appears you're desperately seeking credit.

Soft inquiries, in contrast, are the silent observers of the credit world. They're present, but they leave no trace on your credit score, allowing you to check your own credit or receive pre-approved offers without fear.

A Story from the Archives

Let me tell you about a friend, Alex, who was obsessed with finding the perfect credit card. Alex applied for every card under the sun, racking up hard inquiries like they were going out of style. Soon, Alex's credit score began to wane under the weight of these inquiries. It was a hard lesson in the importance of being selective and understanding the impact of those inquiries.

Embracing a pay-after-deletion model for credit repair is a strategic move that aligns your financial contributions directly with the positive outcomes on your credit report. This approach ensures that you're compensating for success, incentivizing the credit repair service to work diligently towards removing inaccuracies and negative marks. Opting for pay-after-deletion offers a transparent, results-oriented pathway to improving your credit score, providing a sense of fairness and accountability in the credit repair process. It's a method that prioritizes actual, measurable improvements, making it an indispensable option for those looking to invest in their financial future wisely.

GET A FREE QUOTE TODAY

Contact Us

Address:

407 Jackson Park Rd

Kannapolis, NC 28083

(By Appointment Only)

Phone

Tel: 813-345-4097

Text: 813-345-4097

Business Hours-

Monday - 8am - 7pm

Tuesday- 8am - 7pm

Wednesday - 8am - 5pm

Thursday - 8am - 7pm

Friday - 8am - 7pm

Saturday - 8am - 7pm

Sunday - closed